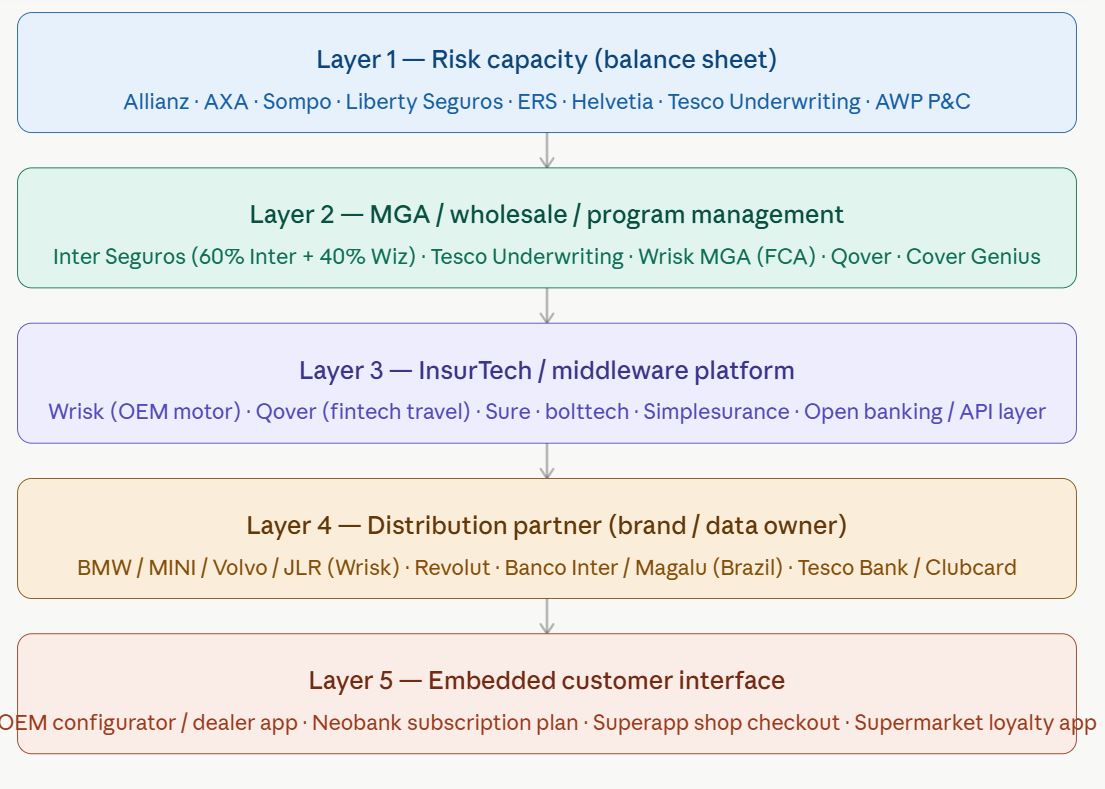

First let's start with the UK, Europe, LATAM and USA before looking how African Telcos have leapfrogged banks in Africa. The reason is that the model deployed in Western markets is not suitable; in fact unworkable. The MVNE/MVNA are operating in the model below but hidden in the infrastructure. Think Gigs enabling Klarna, Revolut and Tide to become MVNOs. Tye conergence of MVNOs and Fintechs will be slower in mature markets as ecosystem integration is already practical. I raise the question as to whether that will change in the future as companies see the innovation leapfrogging already evident in Africa.

Western Infrastructure and layers

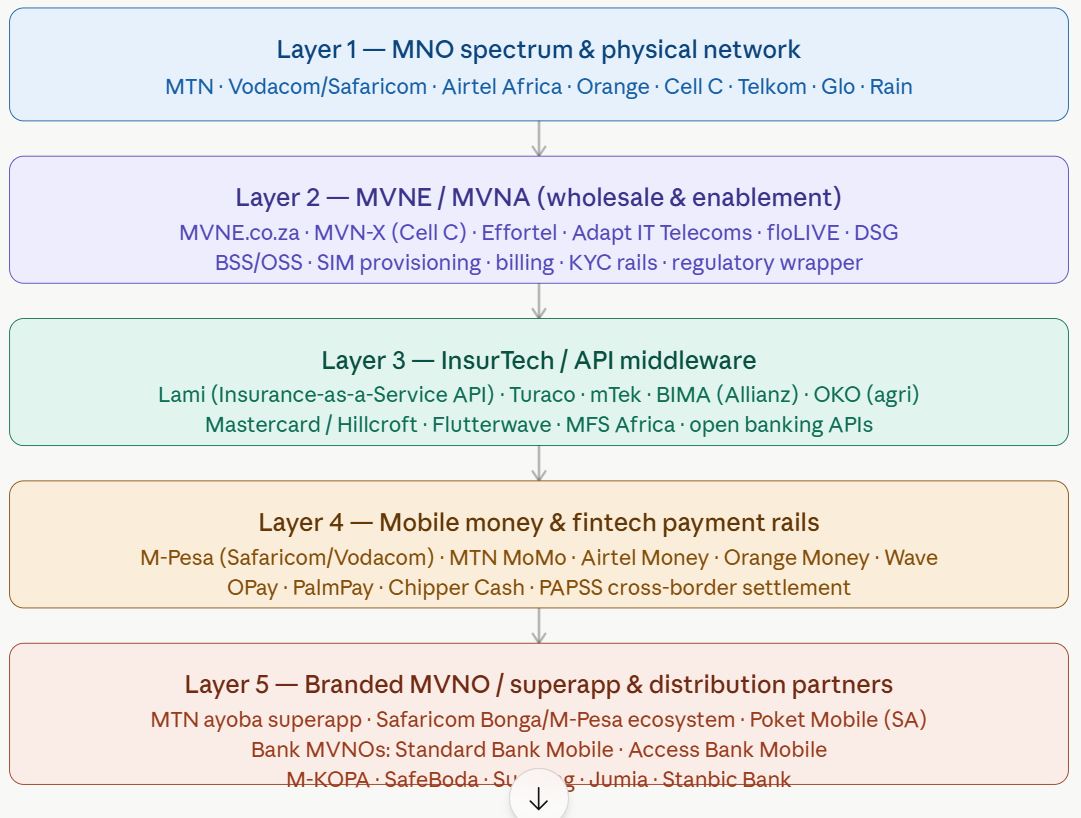

The African model is fundamentally different from the European, Americas one not least because millions of people cannot access a bank acount as there is no local branch and patchy internet coverage. Africa has adopted a MNO/MVNO-centric model, with the telco layer acting as both the infrastructure AND the distribution rail, with the mobile virtual Network enabler (MVNE) connecting and integrating an MNO and branded MVNO.

Insurtechs like Lami, Turaco, mTek (now a part of Boltech which is strong in the European and US geographies) sitting at the middleware layer. The African stack has a fundamentally different shape to the European/Brazilian model — it's six layers rather than five, because the MVNE/MVNA tier is structurally critical in a way it isn't elsewhere. Here's how each layer works in the African context:

African MVNO/MVNE and Insurtech infrastructure and layers

Layer 1 — MNO spectrum and physical network

This is the foundation, but in Africa the MNOs are doing something European operators aren't: they are actively enabling a wholesale MVNO ecosystem; rather than viewing virtual operators purely as competition connecting as partners. MVNOs operating across multiple countries face a significant hurdle — the need to integrate separately with each MNO — resulting in a fragmented model that is technically complex, time-consuming, and costly. The key MNOs are MTN (present in 18+ markets), Vodacom/Safaricom, Airtel Africa, Orange (dominant in Francophone Africa), and Cell C/Telkom in South Africa.

Layer 2 — MVNE / MVNA (the critical African differentiator)

This is the layer that makes the stack work at scale and is what most distinguishes Africa from other markets. The MVNE provides the BSS/OSS platform, SIM provisioning, billing, KYC rails, and regulatory wrappers so that a bank, retailer, or fintech can become a branded MVNO without building telco infrastructure. A growing number of MVNOs are being launched by non-telco players such as banks, retailers, and fintechs — reflecting a broader shift toward bundling mobile connectivity with digital services. Cell C was a pioneer here — it was the first South African MNO to formally enable MVNO rollouts using its MVNE partner MVN-X. South Africa's MVNO industry, valued at USD 90.91 million in 2025 with projections reaching USD 132.34 million by 2030, could double its subscriber base — potentially hitting 10 million SIMs by 2028 — delivering value through hyper-personalised plans and embedded financial services.

Everything Gigs is building in Western markets, Melon Mobile (through Melon Digital) is building in Africa - and Africa is not behind. In some respects, it is arguably further ahead.

Melon Digital is the MVNE platform spun out of Melon Mobile, South Africa’s digital-first MVNO. CEO Calvin Collett describes it as “a complete digital experience and full telco-in-a-box solution” - a platform that allows banks, retailers, and fintechs to launch branded mobile services without building telecom infrastructure. Backed by Amdocs and Amazon Web Services (AWS), Melon Digital is positioned as Africa’s first fully digital MVNE.

Layer 3 — InsurTech / API middleware

This is Africa's equivalent of Wrisk or Qover in the West — but built for very different constraints (USSD, low-data environments, micro-premiums). The leading players:

Lami operates as a white-label Insurance-as-a-Service API. Through a single API, partners can offer health, life, and motor coverage within existing customer journeys with no licences, underwriting setup, or claims infrastructure required. It runs a SaaS platform connected to over 15 African insurers, with clients including Stanbic Bank, Jumia, and Sendy.

Turaco takes the partnership-embedding model. Through its API distribution system, Turaco embedded hospital-cash and micro-health insurance into device financing, savings apps and gig-worker platforms. Its partnership with M-KOPA crossed the one-million-customer milestone. Critically, 90% of Turaco's customers had never bought insurance before — demonstrating the protection gap opportunity.

mTek (Kenya) focuses on paperless, fully digital insurance, and recently partnered with Mastercard to roll out embedded insurance in East Africa.

OKO solves the agriculture vertical specifically, distributing parametric crop insurance to farmers via partnerships with mobile operators — accessible on a basic USSD menu.

Layer 4 — Mobile money and fintech payment rails

This layer has no real equivalent in the European stack — it's what makes embedded insurance financially viable in Africa having taken a decade to mature. The Big 4 — M-Pesa, Airtel Money, MTN MoMo, and Orange Money — collectively underpin Africa's digital economy, support fintech startups, and generate billions in revenue annually. MTN MoMo alone processed 11.1 billion transactions worth $212.2 billion in H1 2025, with 63.2 million active wallets. The mobile money wallet is simultaneously the premium collection mechanism, the claims payout rail, and the identity verification layer for insurance — all in one.

MTN is now structurally separating this layer: MTN aims to build a pan-African "super app," competing with B2B players like Flutterwave and disruptors such as Chipper Cash.

Layer 5 — Branded MVNO / superapp distribution

This is where the convergence happens. Non-telco brands — banks, retailers, gig worker platforms — are using MVNE rails to become MVNOs, bundling connectivity with financial services including insurance. A bank MVNO (like Capitec Connect,, Standard Bank Mobile, FNB Connect) model in South Africa) owns the customer relationship, the transaction data, and the SIM, creating a three-way data flywheel of spending behaviour, mobile usage, and financial history.

The MTN ayoba superapp was the most advanced expression of this innovation — centred around content, gaming, and messaging to drive user engagement, but layered with MoMo payments, credit, and insurance underneath.MTN is foldimg ayoba to simplify in its digital.It was too complicated and MTN is withdrawing it. There was not enough utility value for customers a warning for new entrants to the maket.

APIs are the quickest and easiest way to enable integration across Africa's fragmented MVNO and payment landscape — without them, collaboration between banks, fintechs, and MVNOs stalls.

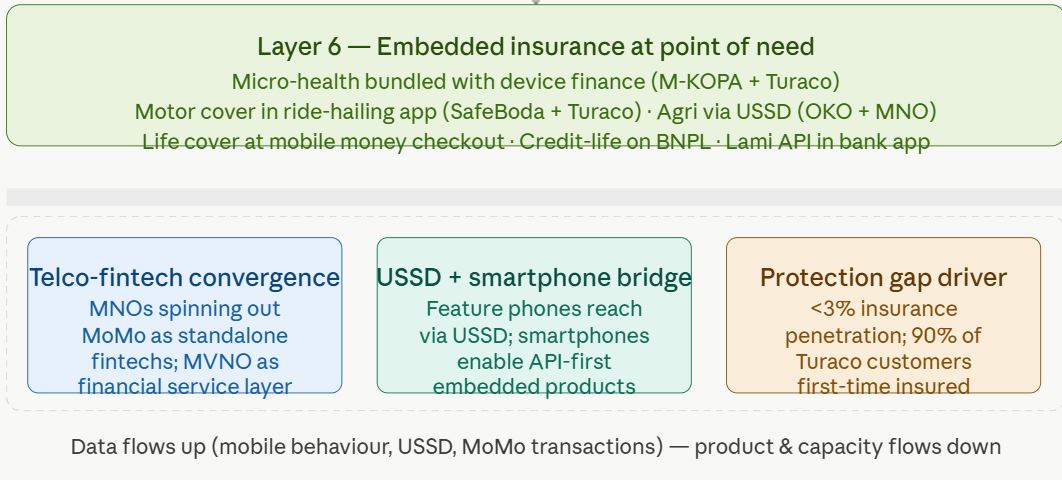

Layer 6 — Embedded, Parametric & Micro insurance at point of need

The end state: insurance that is triggered by a transaction, a device activation, a ride booking, or a harvest registration — not a standalone purchase. The protection gap is stark: insurtechs like Lami Technologies and Turaco are targeting API-based integrations with gig platforms, while competitive intensity will increase as pan-African fintechs scale cross-border operations. The three convergence forces at the bottom of the diagram capture what makes this market unique — the telco-fintech convergence, the USSD-to-smartphone bridge that reaches both feature phone users and smartphone owners, and the massive first-time-insured opportunity that doesn't exist in saturated European markets.

So much to play for; once these new partnerships create a bundle of long-term utility in addition to valued voice/data and IP services the new MNO/MVNO/Fintech & Insurtec entities can build a moat to defend against ther newcomers. The moat being the high cost i.e.loss of valued and compelling services that a subsciber badly wants.

Back to the traditional western model. Will the African innovations prove disruptive? The incumbents may well discount the African model but at the very least they should analyse and compare with how they deliver services. Teco Retail, with its Loyalty Clubcard ( a golden realtime data mine) has its own MVNO Tesco Mobile powered by MNO BT and with Tesco Underwriting offers insurance to customers. Combined with Tesco Bank ( separate company same brand logo) it offers credit cards, loans and savings. But the moat does not appear unbreachable.

In Europe Revolut has built its own banking OS and partners/integrates insurance and banking services. It launched its own MVNO; will subscribers' phones offer a superior CX and range of fintech services to win Tesco customers?

This picture is being drawn acros the UK, Europe, North America and LATAM. Best to not be left behind!

Proof of Identity, Proof of Intent, Agentic Processes

This will be the basis of further articles but a vital part of the planning, strategy and scaling/operationalising of the services described above. Current idenity validation with pin numbers and authenication services have served Mobile Money well. Banks like Revolut incorporate identify validation processes at point of sale. BUT- the operationalisation of Agentic Processes and Digital Workers is a challenge to these systems. Regulators across North America, LATAM, Europe, Asia and Africa are demanding that all players provide fully auditable validation of who made what decisions, on what criteria, when and how.

Not theoretical- mandatory specific compliance.

Validation of Identity MUST be combined with Proof of Intent to have initiated a payment, a purchase, a transaction, an acceptance or rejection…… Digital Agents are not legal entities, neiher human ones. Enterprises, whether banks, insurers, BNPL loans companies, payments rails, - you name it; they must be able to demonstrate proof of intent.

In mature Western and Asian markets the major players seek to address this eg Google with AP2 and Mastercard. But these expensive business models may not be suited for Africa. Look out for companies already delivering identity validation like BillionsNetwork, Strata and Basis Theory. ReLeaf Financial tackles Proof of Intent.

As new business and operational models deploy across Africa keep an eye on the potential for these to upset the apple cart in the Americas, Europe and elsewhere. More on this in later articles

Further Reading

Mike McLaren ‘Why every major Fintech is now becoming a mobile operator’

Allan Rasmussen ‘MNO & MVNO Partnerships: From Old Fears to New Revenue’

Alvin Korkie 'MVNO Blueprint for Africa: The Complete Strategic Framework

While African operators face headwinds, including regulatory complexities and infrastructure gaps, the opportunities in the industry far outweigh the obstacles. The continent’s growing population, expanding digital landscape, rising demand for mobile services, and emerging appetite for new technologies allow the telco sector to leapfrog outdated infrastructure and create new value for businesses and consumers alike. But in a classic case of “What got you here won’t get you there,” telco strategies of today may not be sufficient to win the future.

unknownx500

unknownx500

/Passle/5936d4a43d94760a145c92a7/SearchServiceImages/2026-06-29-17-04-28-162-6a42a59c09492a01ef31fadb.jpg)