Back in 2017 McKinsey flagged the potential to add considerable incremental revenues to mobile subscriptions and I quote from its 2026 report on the same opportunities (Link at bottom article). Mike McLaren describes African NeoBanks Capitec and Jambo Pay adding 35% to 42% revenue upllift as an incentive to other banks..

It took a decaade for mobile network operators (MNOs) Safaricom and MTN to establish Mobile Money enabling people without access to banks the ability to make and receive digital payments. Today Mobile Virtual Network Operators (MVNOs) and Enablers (MVNE) can accomplish this in months and, what's more, create fintech and insurtech ecosystems delivering customised products to large and small niche markets. How about a 112m subscriber user base!

Revolutions tend to be evolutionary over time before suddenly scaling leaving the unaware stranded.

Just look at some of these growing ecosystem partnerships.

- Neobank Nubank (Brazil) launched its own mobile virtual network operator Nucel adding 112 Million subscribers all with a need for loans, savings, insurance as well as phone subscriptions. A 112mill customer for fintech!

- NeoBanks Revolut and N26 have all launched MVNOs and Monzo announced such a venture- this a real wave and not a whim.

- Sezzle a 'Buy-now pay-later (BNPL) company announced a 5G subscription service and its shares rose over 35% in a day

- Established BNPL Klarna announced its own MVNO last year

- Neobank Capitec in Africa together with JamboPay and Rain all have MVNOs, rapid growth

- TIDE offers banking services to 14% of UK SMEs powered by MVNE Gigs which also counts Revolut as a customer

It's not just banks either; Walmart Mexico has its MVNO BAIT offering targeted products to retail customers and Tesco Mobile is the largest MVNO in the UK with the whole of the retail giant's custtomer base potentially buying not just groceries, healthcare products, electricals and drinks but insurance, loans, savings from Tesco Bank.

Enterprises that have a brand loyalty are ideal partners for MVNOs where collaboration can launch highly targeted products and services.

Let's not leave out more traditional mobile network operators (MNOs) . In Africa, Safaricom pionered mobile money service M-PESA, and MTN MoMo ; that continent is the most advanced in giving subscribers digital payment services via their phone mobile wallets. Customers without access to bank account can sell market produce, and services and receive secure and raid payment all from their phones. Taxi drivers take payments, street sellers sell food.

These customers can also access micro loans, micro insurance and other necessities owner-run businesses neeed to sell produce and buy materials. It did take a decade to deliver this innovation and that is the danger for MNOs.

They have to maintain and extend complex infrastructure which delays new innovation. All the while the MVNOs free of such shackles create new financial ecosystems with Fintechs and Insurtechs. MVNOs must ‘rent’ spare capacity from MNOs of course and those partnerships offer viable longevity.

Why can't Fintechs lead this charge? The costs of acquiring new customers is prohibitive when margins are tight. Mike McLaren quotes a typical acquisition cost of $1,450 per customer in 2025. The cost is marginala when offered via a MVNO distribution channel.

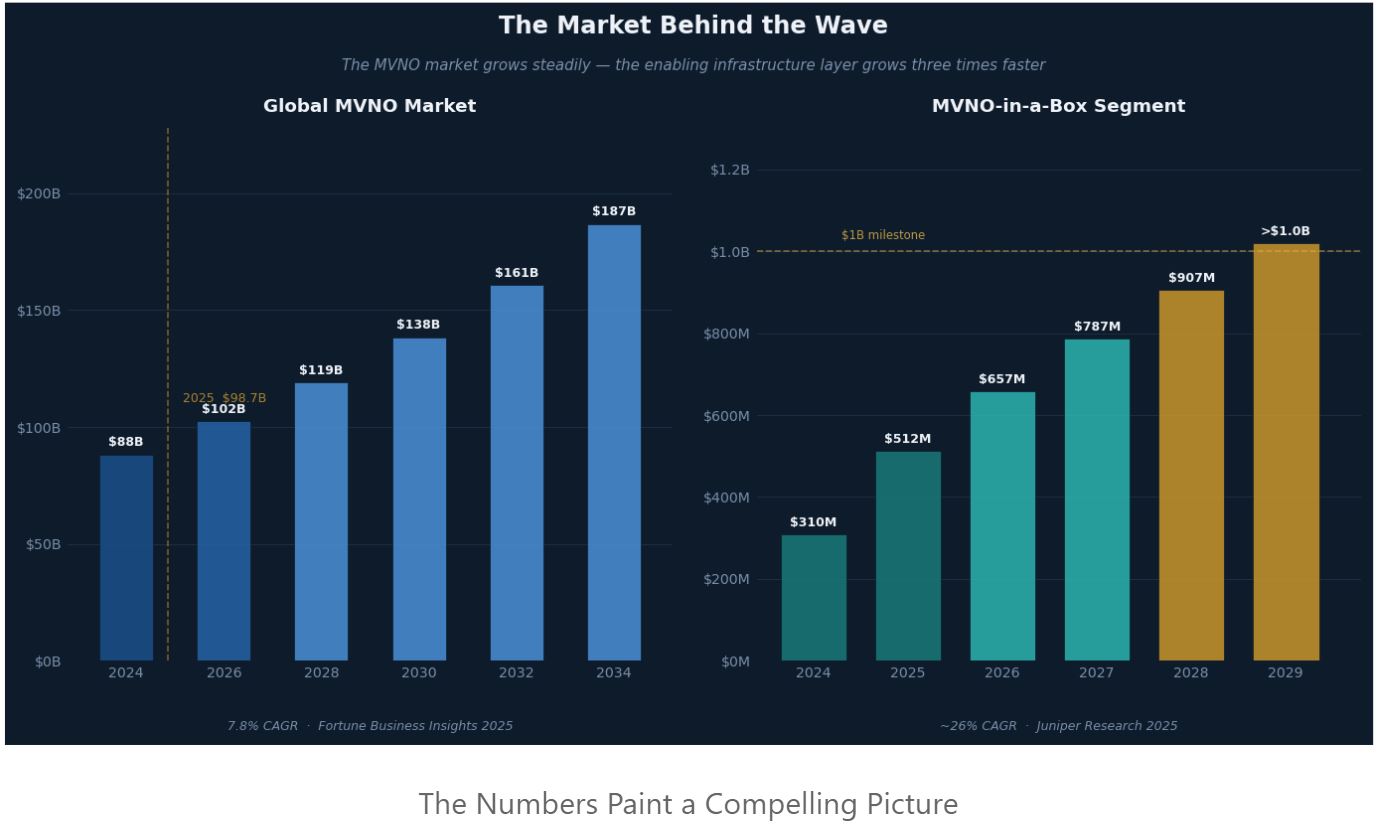

The combination of MNOs, MVNOs, MVNE (enablers) now make ‘MVNO in a Box’ an innovation enabler. The growth rates from Junioer Research tell their own story.

Africa is at the forefront of this trend with established companies like Capitec with MVNO Capitec Connect having proved the market potential. They already face new competition from MVNO Mobile Melon and its MVNE arm Melon Digital applying the Gigs business model proven in western markets with Klarna, Sezzle and Tide. The mindmap of overlapping partners, evolving ecosystems and acquisition is ever changing and well documented by these key people: -

Mike McLaren ‘Why every major Fintech is now becoming a mobile operator’

Allan Rasmussen ‘MNO & MVNO Partnerships: From Old Fears to New Revenue’

Alvin Korkie 'MVNO Blueprint for Africa: The Complete Strategic Framework

These articles give you a comprehensive review of the state and future of the MNO, MVNO, MVNE and MVNA distribution channels. I have sought to look at these through the lens of Fintechs and Insurers. Industry leaders have long urged banks and insurers to think of the customer first, design and customise products for current and unmet needs. And make the customer experience world class and ultra convenient whilst secure. Phones are that front end- people,scan them 60, 100 and more times a day.

Revolut can combine share dealing, risk cover, loans and savings and much more alongside the banking servives it offers. As can the other nweobanks described.

This is a global movement from LATAM through North America to Africa, the Middle East and Asia .

The Chinese have for long taken for granted the ability to manage their private and business lives from their phones. eCommerce platform Alibaba combined with Alipay is a ‘Super-App’ delivering every sort of purcasing, banking and financial/insurance services.

Allan Rasmussen poinbted out to me that Chinese MVNOs do NOT make money on the MNO caopacity they lease ( legislation) but make theorn money on the incremental revenues and profits of the financial/insurance services. A lesson for MVNOs elsewhere.

It is exciting to see the pathfinder role Sub-Saharan Africa has taken with mobile money from MNOs through four NeoBanks pioneering MVNO-Fintech innovation. Africa has learnt to innovate with scare resources unlike Europe and North America used to bloated margins.

Fintechs and Insurtechs should add this global distribution channel into their Go to Market strategies if they don't want to be left behind. Banks and Insurers likewise.

/Passle/5936d4a43d94760a145c92a7/MediaLibrary/Images/2026-08-07-09-53-46-209-6a75ab2a67694a002637d3de.jfif)

/Passle/5936d4a43d94760a145c92a7/MediaLibrary/Images/2026-07-30-08-33-33-453-6a6b0c5db33c106191ff0cfa.JPG)