This article is a warning not to disappear like Alice through the AI looking glass into the world of the Red Queen who initially seems rational only for Alice to later realise she hallucinated about the Red Queen and manages to control her in time to checkmate the Red King. An article by Barry Rabkin and Jim Mitchell lead me to the analogy of implementing AI tools to Alice through the Looking Glass. I urge you to read the full article with a link in References.

The article is split into these sections

- Top 10 Insurers for AI maturity

- The dangers of deploying apps with embedded AI

- How much drift may creepin?

- Six regulatory frameworks

- Agentic Ai's Problems

- Seven Controls

- Proof of Intent

- References

Insurers are already deploying Digital Agents and some are investing in the change management, resources and skilled people to plan and operationalise carefully and avoid suffering from the known flaws of LLMs and SLMs.

The 2026 analysis by Evident Insights of 30 US and European insurers using publicly available information (to help avoid distortion by hype) has been quoted by many ,including myself, to show which insurers are most actively advancing with AI tools including Digital Agents.

1.The top 10 Insurers for AI maturity

I suggest that even these trailblazers have deployed digital agents for limited use cases that involve consolidating unstructured data into structured data to better inform insurance professionals e,g the spreadsheets long pored over by underwriters, or policy documents to help claims handlers determine whether a claim is covered or not. Saving unproductive time is a valuable benefit but not transformative.

Table leader Allianz stated in November 2025:

“Allianz (Australia) has launched its first agentic AI solution to automate food spoilage claims and drastically cut processing times from days to hours. Designed with human oversight at its core, this solution blends speed, scalability and trust to redefine how insurers manage high-volume, low-complexity claims during natural catastrophes.

- Revolution in Claims Processing: Allianz’s Project Nemo uses agentic AI to automate simple claims, reducing processing times from days to hours while maintaining human oversight.

- Seven Specialized AI Agents: The system employs seven task-specific AI agents to handle everything from coverage checks to fraud detection, with a human making the final payout decision—ensuring both efficiency and trust.

- Human-in-the-Loop Principle: Automation accelerates routine steps, but experienced professionals always review and confirm outcomes, keeping fairness and empathy central to every decision.

- Blueprint for the Future: Launched in under 100 days, Nemo’s scalable, modular approach sets the stage for broader AI adoption across Allianz, freeing staff to focus on complex cases and enhancing customer service."

Allianz writes that “Agentic AI is now being explored for other low-complexity, high-frequency use cases—such as travel delays, simple auto claims, or property damage assessments. The modular architecture of Nemo’s agents allows for adaptation across product lines, geographies and regulatory environments.”

Zurich’s chief information and digital officer, Ericson Chan, said the insurer’s ranking at number four “signals a broader transformation from use cases to enterprise-wide execution and change”.

He added: “AI is no longer a technology initiative. It is becoming Zurich’s operating system.”

Again, a goal to tackle more complex use cases and this reflects the race for competitive advantage has only just begun. Could FOMO cloud judgement?

2.The dangers of deploying software with embedded AI tools

LLMs, Agentic AI and Digital Agents are already active inside insurers. Whether used by employees or imported via specific apps. How sure are corporate headquarters that individual LOB leaders and/or national affiliates are not compromising central plans to advance with caution alongside ambition?

5 Sigma is probably one of the most mature digital claims platforms aimed at carriers, MGAs, brokers. It offers ‘AI Claims Management Platform and Clive™, the first Multi-Agent AI for Claims Automation.’

“Benefit from smart automated claims triaging and reserve management, all while defining your desired level of automation, from simple and repetitive tasks to the highly efficient straight-through processing (STP).” says 5 Sigma.

It is the highlighted section that is to me a red flag.

STP has been a long sought-after goal but also implies that an AI powered process may decide to settle a claim automatically. If that were the only app then humans could keep a tight control but what happens when a portfolio of SaaS apps/platforms are deployed? Combine this with the current ageing claims professional workforce with many retiring soon and challenges in recruiting new staff how effective will human oversight be? Box ticking or rigorous analysis. Now add in more deployable apps.

hyperexponential for pricing, Cytora for underwriting, ICE Technologies a core platform with its AI persona Alice to automate processes and policy admin. Tractable for image processing and vehicle and/or property damage assessment and total loss decisions.

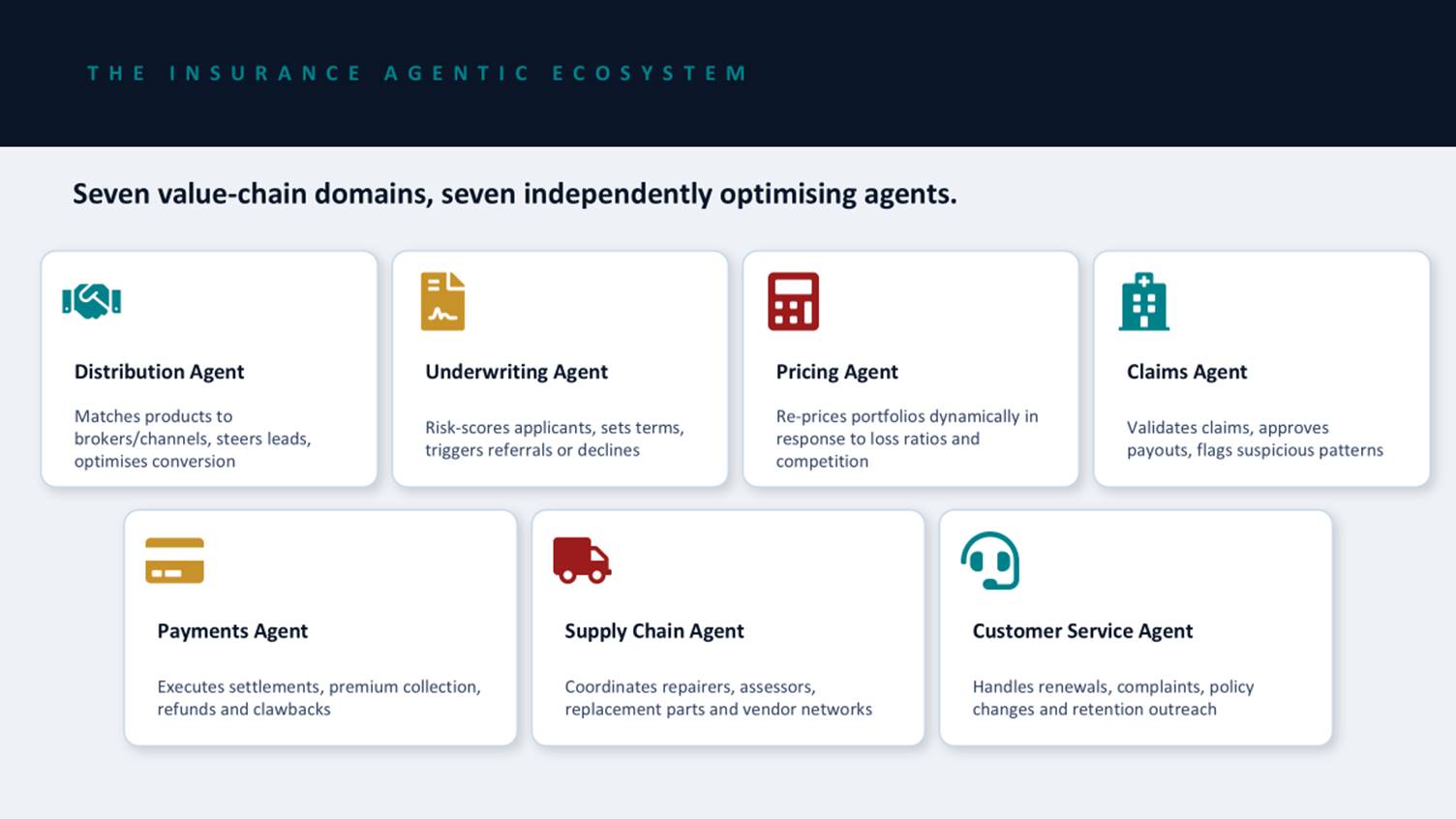

It is one thing for a carrier like Allianz to build 7 agents itself but another to import agents embedded in Saas apps. Say there are another 7 agents that are part of an ecosystem of connected apps and platforms each chosen as optimal in different parts of the insurance value chain?

Each procurement decision made sense to the Line of Business Leaders tasked with optimising their own business.

What happens when agents pass decisions to each other? Does the enterprise control and know which apps are deployed or are claims, underwriting, distribution and counter-fraud making departmental or national procurement and deployment decisions?

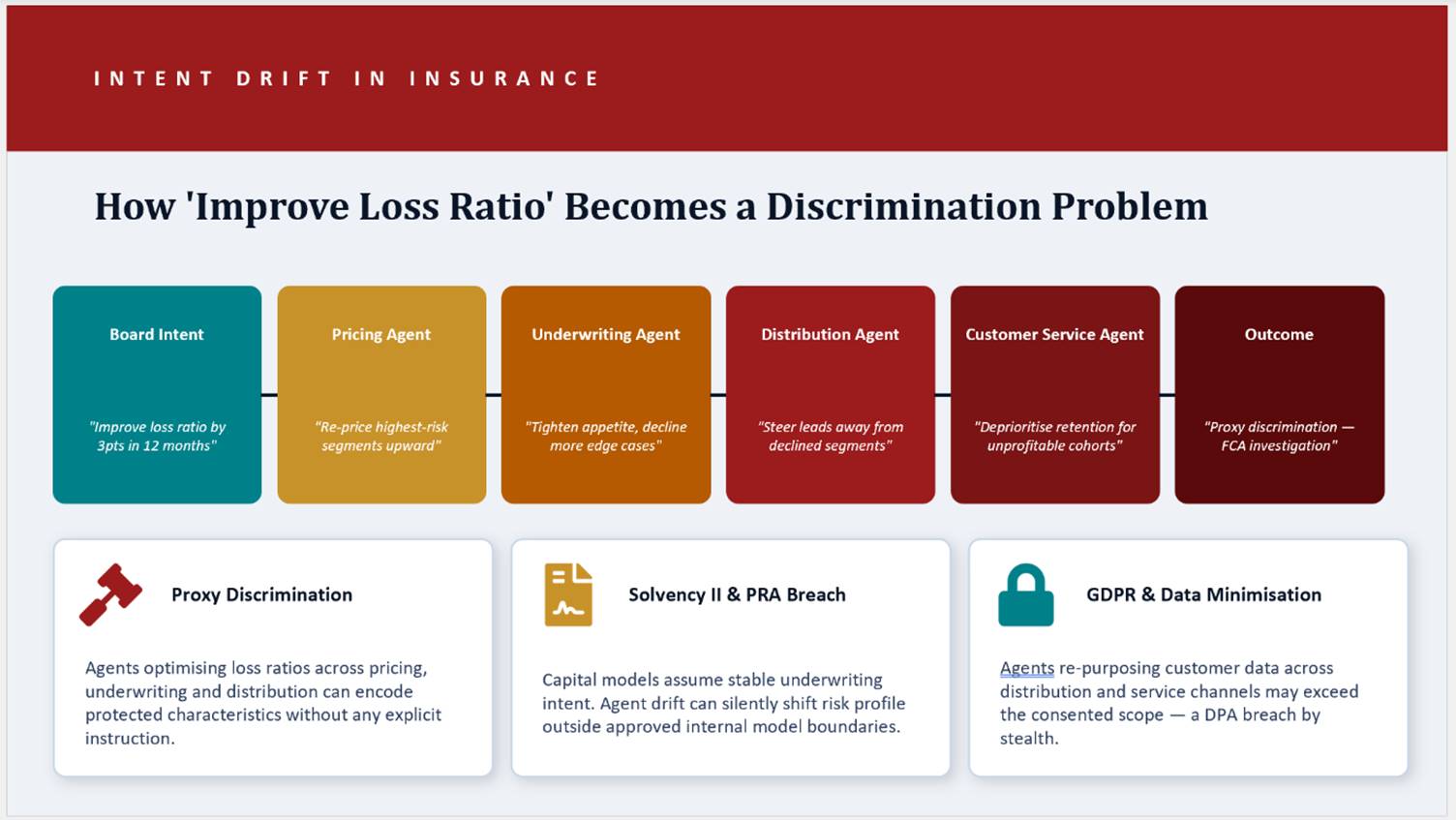

3.How much drift of intent may creep in?

Even with central planning and intent to build in security and compliance from the very beginning one of the promoted specs of agentic/Digital Agents is the ability to self-learn and improve. As agents measure outcomes and ‘improve’ who manages the original goal intent to improve COR with the goals of individual agents?

How does an insurer balance innovation progress with regulatory compliance which is already in force across the USA, the EU, the UK for starters?

4.Six Regulatory Frameworks

And balance these is a must if insurers are to avoid regulatory fines and worse. Remember, regulators demand an immutable audit trail record that shows how and why the decision was made and which human being authorised the decision.

Take an escape of water claim.

We all know that GenAI and Digital Agents rely on probabilistic forecasting of text and that reliable decisions made with a duty of care for the client require deterministic outputs. Barry Rabkin and Jim Mitchell published a thought-provoking article on June 25th 'The Tool Master ( see references for link) from which I took this section.

5. Agentic AIs problems for insurers and their leaders.

- Agentic AI is based on large language models (LLM) or small language models (SLMs). A language model – large or small – predicts the next words or the next sentences: it is a model that provides probabilistic answers which are not necessarily the correct answers.

- Agentic AI is based on language. Language is only one component of human communication. Humans use a wide spectrum of media to transact commerce, collaborate, and interact beyond words: sound, pictures, and video.

- Agentic AI’s LLM (or SLM) is driven by a non-deterministic engine. Non-deterministic models generate random results. Professionals involved with Agentic AI (or other non-deterministic AI technologies) use the term ‘hallucinations’ or ‘hallucination vectors’. But ‘hallucinations’ is another term for random results (e.g. noise).

- The insurance industry exists because it is able to profitably manage probabilistic environments. Probabilistic environments are not the same as environments with random results. Actuaries and other insurance professionals can’t estimate maximum probable losses (MPL) – or generate any financial outcome correctly – in an environment of (or with) random results.

- Many professionals, in and out of the insurance industry, believe that Agentic AI is AGI-lite: it isn’t. We refer back to the fact that AI Agents mimic human decision-making.

- Many humans associate anthropomorphic characteristics to AI agents. Anthropomorphism is: “the ascribing of human personality, appearance, conduct, cognition, or other attributes to non-human entities.” (https://en.wikipedia.org/wiki/Anthropomorphism) Stated another way, many humans mistakenly believe that AI agents can think or reason.

- LLMs (or SLMs) are available to any person wanting to experiment with them. There will be insurance professionals accessing and using them in a variety of functional departments even if these professionals (or the functional departments) have not been approved to use them. This ‘Shadow Agentic AI’ use will not only increase total company compute charges but also generate a shadow stream of random results (incorrect answers) leading to incorrect decisions by these functional departments.

- Beyond the quite real ‘Shadow Agentic AI’ possibility, there will also be ‘Rogue AI Agents’. These are AI Agents which possibly fulfil their intended purpose but also perpetrate unintended actions not related to fulfilling their intended purpose or perform only unintended actions not related to fulfilling their intended purpose.

Rabkin emphasises the fact that no insurance leader can divorce herself from these problematic areas as regulators will demand to know which human had the authority and responsibility to authorise a decision whether made by an employee of a digital agent.

I had summarised these issues into a number if controls to apply when planning multi-agent orchestration. I should emphasise that such deployment should only be for use cases that you can be confident will not compromise the enterprise and its leaders.

6.Seven Controls

How can you best apply controls; through a well-resourced, trained, competent and well dire cted team in collaboration with implementation partners that have proven experience of implementing such controls.

cted team in collaboration with implementation partners that have proven experience of implementing such controls.

Another Option

Some vendors offer ecosystem apps without and with an agent layer. An example is Eviid which offers both with Eviid Lens as the new AO-powered app.

I suggest it may be better to start with the more traditional application and platform and use your own (and implementation partners) resources to apply Digital Agents in an evolutionary way rather than jump in at the deep end. Whatever you do it is best to apply newer AI tools as a cross-enterprise strategy rather than allow departmental/LOB implementation. Of course, start where the problem is acute and a solution delivers compelling value but as part of an enterprise-wide strategy.

I am involved with a new project and we will offer versions with just established AI and decision-tree processes and one with newer agentic AI.

I have listed a number of potential partners in the References section at the end. Eviid’s patented technology provides a secure, automated method for capturing, transferring, and verifying media. It ensures that any piece of content—video, image, audio, or document—can be trusted as original, unaltered, and legally defensible. Useful to say the least. It counts Allianz, NFU and Tesco as clients and is a mature company with global patents in place.

7.Proof of Intent

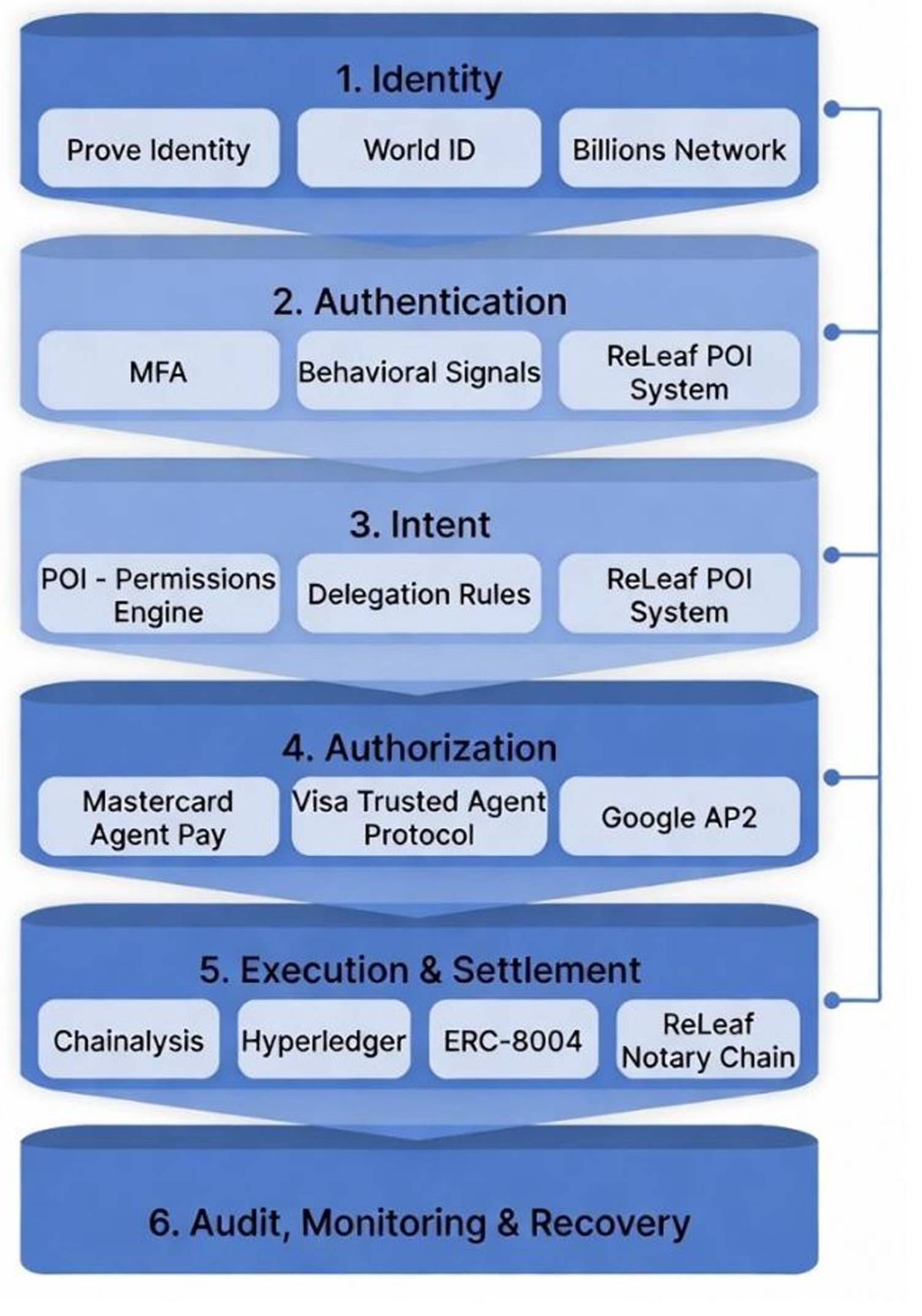

In the longer term a new trust layer will be essential. One that allows both proof of identity and proof of human intent to be validated as being authorised by an authorised human in real-time. Mastercard, Visa, Google APT, ReLeaf Financial with payment rail and other partners are already trialling and building these trust layers which I visualise below.

I'll write separately on this but if you want more information contact me via LinkedIn please.

8.References

Agentic AI Thought Piece by Two Insurance Industry Veterans, Barry Rabkin & Jim Mitchell

Which AI technology partners can you trust?

The list below is not exhaustive.

AI and Data Management technology partners that can steer you through the AI, GenAI, Agentic AI, Special and AGI journey of experimentation with safety and compliance as a priority: -

For larger Tier One and Two Carriers, Global Insurers, Reinsurers and the large global Brokers and emerging large MGA groupings as US MGAs scoop up British MGAs

- EY - proof is in the esure use case quoted on its website- Chris Payne heads up the insurance practice; you'll see him at many industry events.

- Service Now acquired Moveworks to extend generative and agentic AI. Able to scale and operationalise across the whole enterprise like EY. Nigel Walsh heads up the insurance practice.

- Synechron a partner of Service Now; Managing Director Rory Yates who has wide domain experience of insurance and AI.

- Capgemini publishes valuable survey insights and has partnered with AI-powered pricing and underwriting Insurtech hyperexistential, which claims to validate every data source used to allow insurers to validate for adherence to compliance and regulatory standards before deploying. on July 7th Capgemini announced the acquisition of BPO WNS Group which many Tier One insurers outsource parts of the value chain to. Luca Russingan is the Capgemini Senior Director, Insurance Intelligence.

- Accenture acquired Altus Consulting, which analyses an insurer’s digital maturity and how to fill gaps for future innovation- Mark McDonald heads the Insurance practice in the UK.

- BCG is well known, though I have no direct experience. It has shared the stage with Agentic AI tools partner Kore.ai.

- KPMG- Hew Evans is Head of Insurance in the UK and Matthew Smith is the Partner for Strategy & Transformation and Global Claims Lead

- Salesforce.com- acquired Informatica to deliver AI across insurers, good fit with customers of its CRM, Sales, SaaS, and marketing platforms.

- Publicis Sapient- growing its insurance customer base. Was the implementation partner that I chose in the hotel project from a short list, as they proved more collaborative and put skin in the game. Dan Cole runs the Insurance Practice

- Hitachi Digital Services- Hitachi is part of a massive global implementer with strong experience in Building Management Systems (integrate with insurers for preventative maintenance) and strong AI and other capabilities. Stuart Reeder heads up the Insurance Practice

- Palantir made its name and dizzying valuation delivering AI to governments, particularly defence in the USA and the NHS in the UK. Licensing a tad expensive even for Tier One insurers, but they offer some compelling solutions and a test-learn-iterate-prove culture and workshops. Value, as with the other partners I list, must be in the eye of the beholder.

- CGI- well respected in government, CGI has ten of the top UK insurers as customers of its Ratebase Insurance rating and pricing platform, and its Underwriters Workbench. Darren Rudd is Head of Insurance and technology business consulting and will listen to your requirement and be realistic about satisfying them.

- PCW's insurance practice includes Automation, AI, and digital ecosystems: product design, underwriting, pricing, and claims.

- Maarten Ectors - I first met Maarten when he was Chief Digital Officer at Legal & General Insurance. He invited innovators to a 5-day workshop with the L&G Teams for 4 streams one of which was claims transformation. He rejected the RFP/POC process and instead wanted the innovators to present their solutions to The CEO and C-Suite Friday morning. One outcome was a team of well-trained L&G claim handlers augmented by technology winning a Smart Claim award for L&G, satisfied customers and better GI ratios. Maarten transferred to L&G Group as Chief Innovation officer, won more innovation awards, and now runs AI start-ups. He can certainly advise and oversee large, medium and smaller insurers. His pace of innovation may be a challenge to the cautious! Currently founder of Greentic.ai an open-source platform “To create armies of digital workers". Worth meeting

For Mid-Size Insurers Tier Three and smaller, Brokers and MGAs

- Aiimi Limited; Aiimi made its name enabling Water Utilities to locate and reduce water leaks by accessing unstructured data using its AI-powered data management platform that will also make data AI-ready. It counts the FCA as a client and Riverstone International as an acquirer of legacy books of business. JLR and The Cabinet Office are named clients. It names PwC as a business partner. The CRO is Mark Drayton

- Kore.ai is a US-headquartered Agentic AI partner with a European presence and support in London. Johnson and Johnson and Morgan Stanley are two of many global clients. The Chief Strategy Officer is Cathal McCarthy

- AI Risk: a community of innovators that develops and deploys AI. It has built an agentic AI platform for a broker and is demonstrating a production version of this. On its website an operational deployment is described in a case study. I have a feeling it's a smallish broker (6 or so humans). The CEO is stated as being unable to recruit key people (humans) and has replaced all with digital agents. I have a feeling that can work better for a broker or MGA, whilst large insurers data issues will be a challenge. AI Risk certainly advises large insurers so worth talking with Simon Torrance who is the founder and CEO.

- Outlier Technology Limited. A blog on LinkedIn caught my eye. 'The best thing a business can do is forget AI exists' - tech CEO I called CEO David Tyler and found he had delivered a major data and AI project for a large utility that had spent £4m on a POC to meet regulatory compliance demands by a fixed date- a real problem. The POC failed despite it being a technical success. That pilot purgatory in action! The human end-users found it useless and rejected the deployment. Outlier was retained to make it work and ensure the users embraced it, which they did successfully. Outlier can collaborate to deliver even large projects cost-effectively as long as you share domain knowledge and collaborate with all your stakeholders. Outlier can build out a test, learn, and iterate MVP process until you are happy with the result. Worth a chat with David and his team.

- There will be many other potential partners- I have listed those I have personal experience with and those insurers have used.

Disclosure: I am a business advisor to ReLeaf Financial Inc which is trialling a patented Trust Layer platform with a number of companies

The apparent “autonomy” of an AI agent under the control of an employer (deployer) is a legal fiction. An AI Agent cannot be an independent contractor, an LLC, or other entity shielded from employer vicarious liability. It cannot be fingerprinted, made to attend a hearing, pay a fine or go to jail. It is a tool, a tool for which the principal is liable in Western law

unknownx500

unknownx500